Resources

Ecosystem Strategy: What is it and How Does it Relate to BaaS and Digital Supply Chain Disruption?

Key Points:

- Identify the industry shift from a traditional market strategy to an ecosystem strategy

- Differentiate between Direct Sales Strategy, Channel Sales Strategy, and Ecosystem Strategy

The year was 2014 and a new payment form factor was evolving, seeded by tech giant, Apple. I was at a major card processor at the time, working on the team responsible for the pilot launch of Apple Pay. We were just one of many branches within Apple’s orchard responsible for bearing fruit. As I hung there, suspended with others in the grove, I realized something…Apple thought differently about bringing products to market.

Apple didn’t just have a supply chain that manufactured their iPhone 6 and a distribution channel of global retail stores to achieve last mile delivery of their iPhones. In addition to the traditional supply chain and distribution channel strategies, Apple also had an overarching ecosystem strategy to drive both the production, usability, and adoption of Apple Pay.

It was this latter strategy that intrigued me. I began researching ecosystem strategies to understand how they differed from traditional market strategies.

In a traditional market strategy, an entity, say a bank, owns the products they offer to their retail and commercial customers. In an ecosystem strategy, various entities contribute a service and/or product to the ecosystem to provide an interconnected offering to fulfill a customer segment need.

- In a traditional market strategy:

- The bank uses suppliers such as core and card processing providers to help them build these products, but these entities are always suppliers of the bank.

- In a 2013 OCC Bulletin, the OCC referred to these entities as Third-Parties and provided banks with guidance for managing risk in these relationships.

- This guidance is now, unfortunately, not comprehensive enough due to the rise of ecosystem business models that have evolved out of BaaS and embedded finance trends. So we now await the OCC, FDIC, and Fed’s inter-agency guidance to Third-Party risk management as a follow on to their joint issuance of proposed guidance in 2021.

- In an ecosystem strategy:

- The lines between third-parties, suppliers and distributors are irrelevant. This is because an ecosystem strategy requires coordinated accountability across all entities.

- Ecosystems operate out of orchestrated, mutually shared interest, as opposed to traditional buyer/supplier relationships.

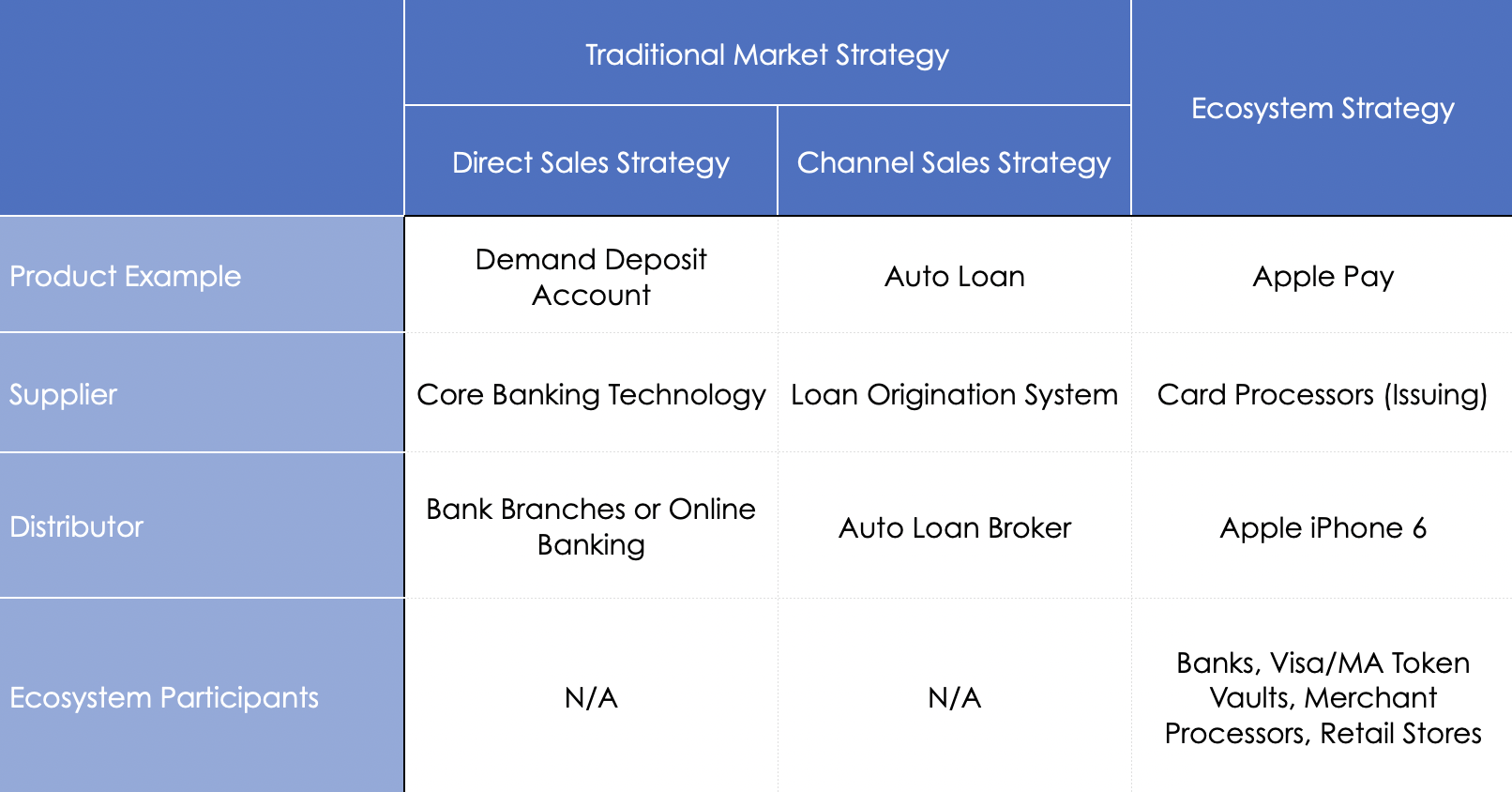

Review the chart below to assess the differences between a traditional market strategy divided into either a direct sales strategy or a channel sales strategy and an ecosystem strategy.

The traditional supply chain is disrupted in an ecosystem strategy. And companies or banks that find themselves in an ecosystem business model—while still applying traditional market strategies—will lose influence within the ecosystem.

It is this concern that triggers in me whenever I hear a bank describe themselves as a supplier to a fintech in a BaaS model. This tells me the bank has never spent time in the Apple orchard, or if they have, they’ve not hung around long enough to recognize they exist in an ecosystem and not a traditional market.

It is critical that banks recognize they’re not a supplier to their BaaS partners or their embedded finance partners. They are co-creating a product together, and everyone is responsible for bearing fruit within the orchard.

My Apple Pay experience taught me a lot about ecosystems. Not just because of the symbiotic relationships that developed as a result of Apple Pay, but also because I learned how to think differently during my tenure in the Apple orchard.

After months of working on the project, I remember telling executives in our company that the Apple folks didn’t just do things differently, they thought differently. They thought differently about buyer/supplier relationships. They thought differently about creating a coordinated customer experience. They thought differently about co-creating products across entities. And above all, they positioned themselves as the key influencer within the Apple Pay ecosystem. They did this even though the primary card products powering Apple Pay belonged to the banks. They taught me that increasing influence is always the priority within an ecosystem strategy.

In my last post, we discussed the cultural and brand impacts digital supply chain disruption has on the banking industry. So I wanted this post to challenge us to think differently about ecosystem business models and their impact on our BaaS and embedded finance strategies. Because digital supply chain disruption always requires an ecosystem strategy.